Yahoo News

Yahoo News How Should Investors Feel About Service Corporation International's (NYSE:SCI) CEO Remuneration?

This article will reflect on the compensation paid to Tom Ryan who has served as CEO of Service Corporation International (NYSE:SCI) since 2005. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Service Corporation International.

See our latest analysis for Service Corporation International

How Does Total Compensation For Tom Ryan Compare With Other Companies In The Industry?

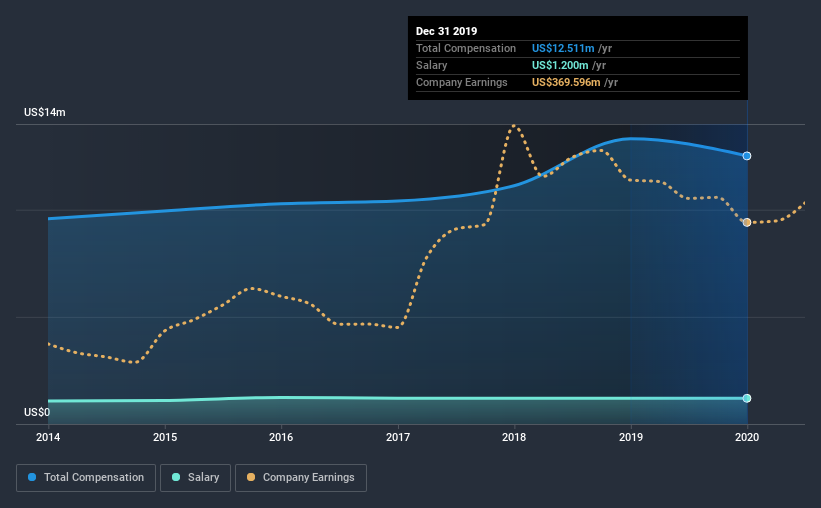

Our data indicates that Service Corporation International has a market capitalization of US$8.0b, and total annual CEO compensation was reported as US$13m for the year to December 2019. We note that's a small decrease of 6.0% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$1.2m.

For comparison, other companies in the same industry with market capitalizations ranging between US$4.0b and US$12b had a median total CEO compensation of US$1.9m. Accordingly, our analysis reveals that Service Corporation International pays Tom Ryan north of the industry median. What's more, Tom Ryan holds US$52m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

Component | 2019 | 2018 | Proportion (2019) |

Salary | US$1.2m | US$1.2m | 10% |

Other | US$11m | US$12m | 90% |

Total Compensation | US$13m | US$13m | 100% |

Speaking on an industry level, nearly 19% of total compensation represents salary, while the remainder of 81% is other remuneration. Service Corporation International sets aside a smaller share of compensation for salary, in comparison to the overall industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Service Corporation International's Growth

Service Corporation International has seen its earnings per share (EPS) increase by 6.0% a year over the past three years. It achieved revenue growth of 1.0% over the last year.

We'd prefer higher revenue growth, but it is good to see modest EPS growth. It's clear the performance has been quite decent, but it it falls short of outstanding,based on this information. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Service Corporation International Been A Good Investment?

Most shareholders would probably be pleased with Service Corporation International for providing a total return of 35% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

As we touched on above, Service Corporation International is currently paying its CEO higher than the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. Importantly though, shareholder returns for the last three years have been excellent. That's why we were hoping EPS growth would match this growth, but sadly that is not the case. We'd ideally want to see higher EPS growth, but CEO compensation seems to be within reason, given high shareholder returns.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 1 warning sign for Service Corporation International that investors should think about before committing capital to this stock.

Important note: Service Corporation International is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.